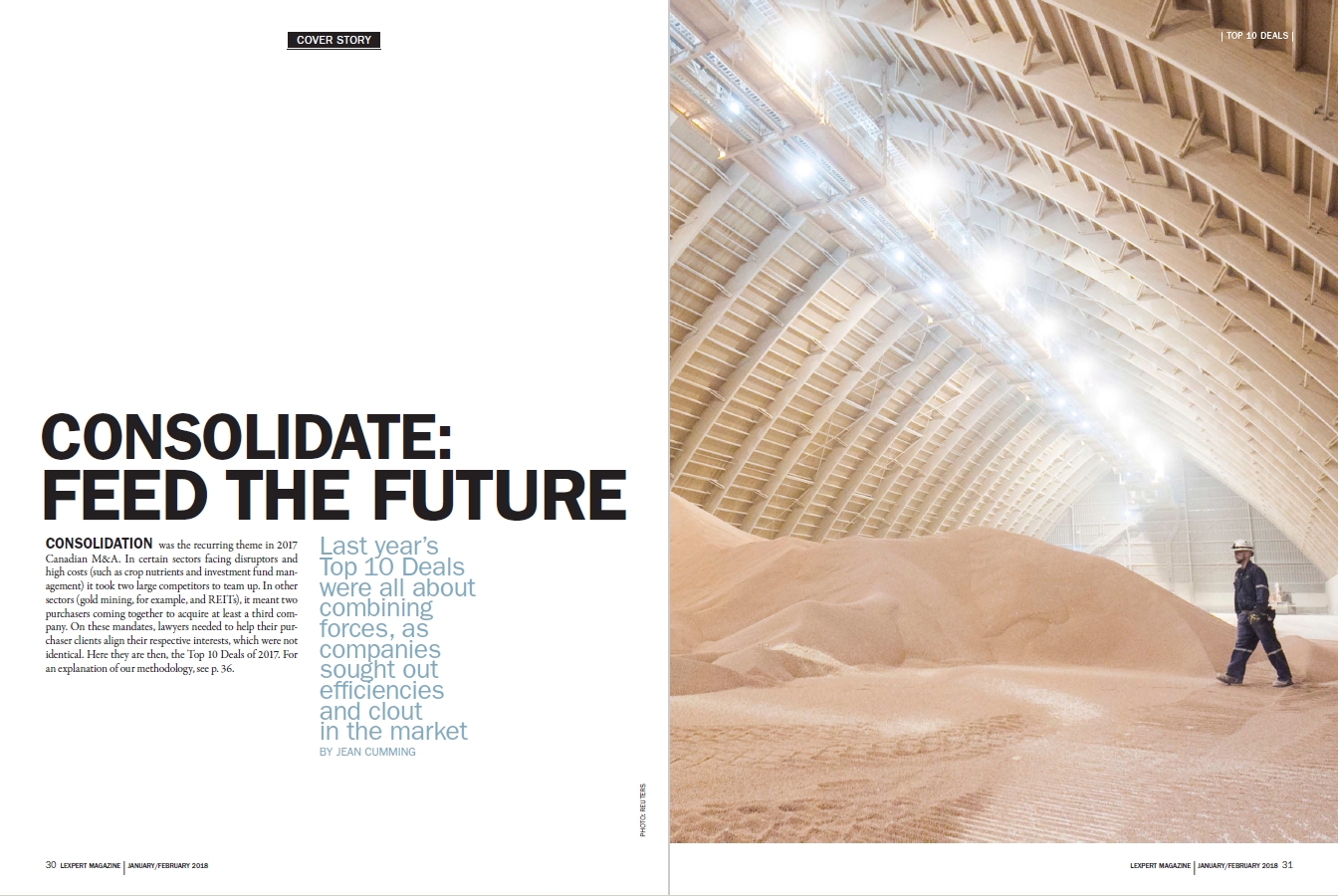

CONSOLIDATION WAS THE RECURRING theme in 2017 Canadian M&A. In certain sectors facing disruptors and high costs (such as crop nutrients and investment fund management) it took two large competitors to team up. In other sectors (gold mining, for example, and REITs), it meant two purchasers coming together to acquire at least a third company. On these mandates, lawyers needed to help their purchaser clients align their respective interests, which were not identical. Here they are then, the Top 10 Deals of 2017. For an explanation of our methodology, click here.

CONSOLIDATION WAS THE RECURRING theme in 2017 Canadian M&A. In certain sectors facing disruptors and high costs (such as crop nutrients and investment fund management) it took two large competitors to team up. In other sectors (gold mining, for example, and REITs), it meant two purchasers coming together to acquire at least a third company. On these mandates, lawyers needed to help their purchaser clients align their respective interests, which were not identical. Here they are then, the Top 10 Deals of 2017. For an explanation of our methodology, click here.

1. POTASHCORP AND AGRIUM MERGE TO FORM NUTRIEN

This merger of equals was announced by Potash Corp. of Saskatchewan Inc. and Agrium Inc. in 2016, when commodity markets were stagnating, with the anticipation of $500 million per annum in cost savings. The deal closed on January 2, when the newly merged entity, Nutrien Ltd., began trading on the TSX and NYSE. Bill Braithwaite led the team at Stikeman Elliott LLP, which included Mike Devereux, for PotashCorp and its General Counsel, Joe Podwika.

Braithwaite said, “While the deal gave all of us the opportunity to work on the biggest true ‘merger of equals’ in Canadian history, it also gave the deal team a chance to help create — essentially like an IPO — a new western Canada based global giant.” Ross Bentley, who led the team at Blake, Cassels & Graydon LLP for Agrium, said, “This transformational business combination has compelling industrial logic, facilitates the creation of a true ‘Canadian champion’ and will create benefits to the Canadian economy, for customers and employees within the combined worldwide operational footprint of Nutrien, and for shareholders as Nutrien achieves its targeted synergies.”

These two Canadian crop nutrient producers, with some differing and some overlapping products, are global in scale and operation. And so the regulatory hurdles involve several jurisdictions and entities, including the US, China and India. On closing, the two merged to create Nutrien, a manufacturing, wholesale and retail business with an enterprise value of $36 billion. Stocks of both companies rose in the third quarter of 2017.

Michael Kandev, who led the Tax team for PotashCorp at Davies Ward Phillips & Vineberg LLP with Nathan Boidman, elaborated: “Conceptually, a merger of equals can be effected contractually or structurally. The former would see each corporate group remain legally separate but ‘merged’ by contractual agreements including profit equalization arrangements. A corporate-structural merger was instead chosen by PotashCorp and Agrium.

“A corporate merger could be effected in several ways, but ultimately the parties’ commercial and business objectives were best reflected in a structure involving the establishment of a new top holding publicly listed corporation, called Nutrien Ltd., that would directly and indirectly acquire PotashCorp and Agrium with their shareholders emerging as shareholders of Nutrien Ltd.

“As part of the transaction structuring exercise, we had to provide for several critical tax considerations that roughly fall into two categories: ensure that taxable shareholders defer tax upon participating in the merger and that the merging corporations and their executives both defer tax on the deal and have the best tax and corporate-structural platform going forward.”

The deal closing was pushed to the end of 2017 to allow Competition regulators in various jurisdictions to review the deal. According to the companies’ joint press release: In Canada and the United States, the parties worked with the Canadian Competition Bureau and the Federal Trade Commission to resolve final issues in superphosphoric acid (SPA) and nitric acid. The companies have also been informed that the Ministry of Commerce (MOFCOM) in China and, independently, the Competition Commission of India (CCI) conditioned their respective approvals of the proposed transaction on the divestment of certain of PotashCorp’s offshore minority ownership interests.

The remedies under consideration are not expected to impact the estimated $500-million of annual operating synergies. As the largest global provider of crop inputs and services, Nutrien will play a critical role in ‘Feeding the Future’ by helping growers to increase food production in a sustainable manner.

Key Law Firms

PotashCorp: Stikeman Elliott LLP (M&A, Competition/Regulatory); Davies Ward Phillips & Vineberg LLP (Canadian Tax); Jones Day; Alchemy Capital (US Tax Planning)

Agrium: Blake, Cassels & Graydon LLP (Canadian M&A and Competition); Paul, Weiss Rifkind, Wharton & Garrison LLP (M&A), Latham & Watkins LLP (US and Global Antitrust); Felesky Flynn LLP (Canadian Tax); Osler Hoskin & Harcourt LLP (US Tax)

Agrium Board of Directors: Norton Rose Fulbright Canada LLP

2. CENOVUS ACQUIRES CONOCOPHILLIPS ASSETS FOR $17.7 BILLION

Calgary-based Cenovus Energy Inc. was “bulking up in a $17.7-billion deal to more than double its production as the repatriation of Canada’s oil sands winnows control of the resource to a handful of domestic players,” according to The Globe and Mail.

“It would acquire a 50-per-cent interest in the Foster Creek and Christina Lake oil sands projects owned by partner ConocoPhillips Co., giving it full control of the steam-driven bitumen assets in the biggest oil sands deal to date.” To achieve this, Cenovus issued $3 billion in shares in a bought deal and took out $10.5 billion in loans. It also announced it was “jettisoning production equivalent to 47,600 barrels a day (b/d), with proceeds aimed at repaying debt.”

According to Globe reports, the deal can be viewed in this context: “The global energy companies, hit by high debt levels during the downturn, have also been frustrated by high costs, low Canadian crude margins and delays over major pipeline projects billed as key to bolstering economics in the region.”

Pat Maguire at Bennett Jones LLP says, “The acquisition provides Cenovus with full control over its oil sands operations and current and potential future growth projects at Foster Creek, Christina Lake and Narrows Lake, doubles the Corporation's oil sands production, almost doubles its proved bitumen reserves and provides Cenovus an additional growth platform with more than 3 million net acres of undeveloped land, exploration and production assets and related infrastructure in the Deep Basin.”

Jeff Bakker from Blakes, co-counsel to Cenovus Energy Inc., told Lexpert: “This was a transformational acquisition for Cenovus Energy Inc. and was the largest energy asset acquisition ever undertaken in Canada. The aforementioned acquisition bridge facilities were one of the largest bridge facilities ever placed in the Canadian lending market.”

Janice Buckingham, of Osler, Hoskin & Harcourt LLP, counsel to ConocoPhillips, said this “strategic sale to Cenovus was significant not only in terms of absolute dollar value, at $17.7 billion, but in terms of maximizing value in a low-price environment. This was achieved by combining cash consideration with share consideration and anticipated upside in pricing that provided a win for both parties, while ensuring each party could extrapolate value from remaining interests.”

Key Law Firms

Cenovus: Bennett Jones LLP (Lead M&A); Blake, Cassels & Graydon LLP (Co-Counsel, Lead Finance); Paul, Weiss, Rifkind, Wharton & Garrison LLP (US M&A)

ConocoPhillips: Osler, Hoskin & Harcourt LLP; King & Spalding LLP

Underwriters: Norton Rose Fulbright Canada LLP

3. BCE ACQUIRES MANITOBA TELECOM SERVICES

In March of 2017, according to the company’s press release, BCE Inc. “announced the launch of Bell MTS following the completion of its acquisition of Manitoba Telecom Services (MTS). Uniting the local and national strengths of MTS and Bell Canada, the new Bell MTS will bring unprecedented investment and innovation in broadband communications to Manitoba, including the rollout of next-generation Fibe services and Canada’s fastest-ranked wireless network.”

The $3.1-billion deal closed after considerable efforts on the regulatory side. According to BCE, upon completing the transaction, it picked up a total of 710,000 wireless, TV and internet customers. Because Manitobans had lower wireless prices than elsewhere in Canada, BCE needed approval from the Competition Bureau and the federal Department of Innovation, Science and Economic Development. According to the Globe, “BCE agreed to transfer 24,700 of its wireless subscribers (plus cellular airwaves and retail stores) to rural Internet provider Xplornet Communications Inc., which plans to launch a new mobile business in the province. BCE had already agreed to transfer subscribers and stores to Telus, which will pick up 110,000 new wireless customers as part of a $300-million side deal.”

Winnipeg will serve as BCE’s headquarters for the provinces of Manitoba, Saskatchewan, Alberta and British Columbia. Faced with a maturing telecom industry, BCE has made various acquisitions. Blakes was Competition counsel to BCE, led by Brian Facey, who told Lexpert, “As part of the deal, Bell MTS will invest $1 billion over five years to upgrade the wireless network to LTE advanced and build fibre connections (a significant upgrade in the technology for the people in Manitoba).”

Key Law Firms

BCE: McCarthy Tétrault LLP (Corporate/M&A, Telecom/Regulatory, Tax); Blake, Cassels & Graydon LLP (Competition); Sullivan & Cromwell LLP ; Taylor McCaffrey LLP

MTS: Stikeman Elliott LLP (M&A, Competition (Regulatory), Tax); MLT Aikins LLP; Paul, Weiss, Rifkind, Wharton

& Garrison LLP (US M&A)

4. PEMBINA ACQUIRES VERESEN

In its press release, Pembina Pipeline Corp. announced the completion of its transaction with Veresen Inc. pursuant to a plan of arrangement under s. 193 of the Business Corporations Act (Alberta) “to create one of the largest energy infrastructure companies in Canada.” Pembina acquired all of the issued and outstanding common shares of Veresen in a transaction valued at approximately $9.4 billion, including the assumption of Veresen’s debt (including subsidiary debt) and preferred shares. As described by Chad Schneider of Blakes, which was counsel to Pembina:

“The transaction creates one of the largest energy infrastructure companies in Canada and expands Pembina’s reach in the United States, including potentially entering the offshore LNG market with its proposed Oregon Jordan Cove project. It also creates an organization of meaningful scale able to pursue larger growth projects and an emerging competitor to established national and North American infrastructure companies headquartered in Canada. The combined company will have a strong position in the Western Canadian Sedimentary Basin, home to the world’s third-largest crude reserves.”

Mick Dilger, Pembina’s President and CEO said: “With increased size and scale, the combined companies create a platform in which we can pursue expanded growth opportunities while continuing to support future dividend growth and value creation for our shareholders. Our customers will also benefit from the enhanced service offerings through the highly integrated asset base and the extended geographic reach.”

Key Law Firms

Pembina: Blake, Cassels & Graydon LLP; Bracewell LLP (US Counsel)

Veresen: Osler, Hoskin & Harcourt LLP

5. CI FINANCIAL ACQUIRES SENTRY INVESTMENTS

CI Financial Corp. acquired Sentry Investments Corp., valued at $780 million in cash and stock, merging two of Canada’s largest independent asset managers. Again, consolidation to face the competition ahead is the strategy, and CI’s press release makes this clear:

“Through the acquisition, CI will add significantly to its mutual fund portfolio, boosting its assets under management by 16 per cent to $140-billion. The deal will also create one of the largest sales forces in the industry in Canada. ‘Scale is a clear advantage,’ CI Financial chief executive officer Peter Anderson said. ‘There are not a lot of large asset managers in the Canadian market today.’”

As the Globe reported, “The deal comes in the midst of difficult period for the mutual fund industry as exchange-traded funds grow in popularity. While mutual funds still have a strong footing in Canada, with more than $1-trillion in assets, investors are increasingly turning to an increasing array of ETFs, which usually come with significantly lower costs.”

Jeff Lloyd of Blakes, which acted as counsel to CI Financial Corp., said, “The deal combined two of Canada’s largest independent active asset-management firms. The acquisition has increased CI’s AUM [assets under management] to approximately $140 billion and total assets [assets under management plus assets under advisement] to approximately $181 billion, and created one of the largest Canadian sales forces in the industry. The transaction involved a concurrent $250-million debenture offering by CI in order to finance a portion of the purchase price, as well as the requirement to obtain an extensive suite of securities regulatory approvals in view of the regulated nature of the industry.”

Key Law Firms

CI: Blake, Cassels & Graydon LLP

Sentry: Davies Ward Phillips & Vineberg LLP

Sentry’s Independent Directors: Borden Ladner Gervais LLP

Underwriters on a related debenture financing: Torys LLP

6. TOTAL ENERGY SERVICES ACQUIRES SAVANNA ENERGY SERVICES

Total Energy Services Inc., a diversified oilfield services company based in Calgary, purchased all of the outstanding common shares of another Calgary-based oilfield services company, Savanna Energy Services Corp., by way of an unsolicited takeover bid on December 9, 2016.

On March 1, 2017, Total filed a Notice of Change and Notice of Variation to the Offer to, inter alia, increase the consideration payable for each Savanna Share to $0.20 in cash plus 0.13 of a Total common share. On March 9, 2017, Savanna announced that it had entered into an agreement with another publicly traded oilfield services company, whereby such company would acquire all of the Savanna Shares pursuant to a plan of arrangement. Notwithstanding this competing transaction, on March 24, 2017, Total acquired 60,952,797 Savanna Shares under the Offer, representing approximately 51.6 per cent of the total number of outstanding Savanna Shares, and extended the Offer to April 7, 2017, in accordance with Canadian securities laws. The Offer was subsequently extended to April 27, 2017.

As of April 27, 2017, Total owned approximately 86 per cent of the issued and outstanding Savanna Shares, which included Savanna Shares taken up by Total under the Offer and Savanna Shares purchased in market transactions by Total after commencement of the Offer. According to Nicholas Fader, a Calgary partner at Bennett Jones LLP, which acted for Total Energy, this “bid represented the first successful unsolicited takeover under the new Canadian bid rules, and those rules have dramatically altered certain aspects of the traditional game plan for unsolicited offers. The 105-day bid period associated with the May 2016 amendments likely influenced Savanna’s decision not to implement a shareholder rights plan, which allowed the bid to proceed without a cease trade proceeding. However, the amended bid regime gave rise to a number of new issues, including the interplay between the bid rules and the shareholder approval requirements of the TSX. The Total Energy bid highlighted the need for additional work on the regulatory front to promote peaceful coexistence between securities laws and exchange rules in the context of share deals.”

Key Law Firms

Total Energy: Bennett Jones LLP; Paul, Weiss, Rifkind, Wharton & Garrison LLP (US M&A)

Savanna: Burnet, Duckworth & Palmer LLP; Dorsey & Whitney LLP (US Counsel)

7. SMARTREIT AND STRATHALLEN ACQUIRE ONEREIT

According to Marketwired’s release, “OneREIT is an unincorporated, open-end real estate investment trust with more than C$1 billion of total assets. It owns and manages 56 properties across 10 provinces and territories in Canada covering 7 million square feet.

“SmartREIT is one of Canada’s largest real estate investment trusts with total assets of approximately C$8.9 billion. It owns and manages 32 million square feet in value-oriented, principally Walmart-anchored retail centres.

“Strathallen Capital is a fully integrated Canadian real estate management company.”

“OneREIT entered into separate agreements with Smart Real Estate Investment Trust and Strathallen Acquisitions Inc., an affiliate of Strathallen Capital Corp., to acquire all of OneREIT’s assets and assume all of its liabilities, including long-term debt and all residual liabilities, whereupon OneREIT redeemed all of its publicly traded units. The Transaction is the outcome of OneREIT’s strategic review process, previously announced in June 2016. The consideration for the Transaction is comprised of cash and SmartREIT units that value OneREIT units at $4.26 per unit on a fully prorated basis. The consideration represents a premium of 14.5% to the August 3, 2017 closing price and a premium of 14.8% to the 20-day volume weighted average unit price ending August 3, 2017. As well, the consideration represents a premium of 22.4% to the unaffected unit price on June 7, 2016, the day prior to OneREIT’s announcement that it would explore strategic alternatives.”

Acting for OneREIT was a Fasken Martineau DuMoulin LLP team led by Jon Levin and including Anil Aggarwal. According to Levin, “In part, the transaction reflects the adverse impact on the Canadian retail real estate landscape of ecommerce, particularly as evidenced by the lengthy and difficult auction process. It was necessary to reconcile competing and often inconsistent objectives of two arm’s length buyers with very different needs and objectives in order to maximize value for the REIT’s unitholders. One indication of the success of this extraordinarily complex deal was the overwhelming unitholder vote of approval.”

Key Law Firms

OneREIT and OneREIT Special Committee: Fasken Martineau DuMoulin LLP (M&A, Litigation, Tax, Competition); Goodmans LLP (Real Estate)

Strathallen: Stikeman Elliott LLP; Minden Gross LLP (Leasing)

SmartREIT: Osler, Hoskin & Harcourt LLP; Davies Ward Phillips & Vineberg LLP

Financial Advisor to the Special Committee of Independent Trustees of OneREIT: Torys LLP

8. THE NORTEL GLOBAL SETTLEMENT

This Top Deal was formerly one of our Top Business Decisions. “I’ve been involved in the Nortel case since the fall of 2008,” says Jay Carfagnini, of Goodmans LLP, which represented the Monitor, Ernst & Young. While Nortel may not have taken quite as long as Jarndyce v. Jarndyce from Dickens’ Bleak House, it drew in many law firms, courts, meetings, and multiple jurisdictions — and has taken a very long time indeed. Torys LLP, which acted for Nortel, with a team led by Tony DeMarinis and Scott Bomhof, wrote to Lexpert, “Nortel’s multi-jurisdictional business, unprecedented legal issues, and eventual big cash stockpile made the restructuring both exceptionally challenging and fascinating, and a case the likes of which may not be seen again for some time.”

Sticking with our consolidation theme, this time globally, the Nortel case/deal was re-fuelled by an infusion in 2011 that took most observers by surprise. As reported at the time in The Guardian, “The Apple, Microsoft, Sony and BlackBerry maker Research in Motion are part of a winning consortium of six companies which have bought a valuable tranche of patents from the bankrupt Nortel Networks patent portfolio for $4.5bn (£2.8bn), in a hotly contested auction that saw Google and Intel lose out.” There was something to settle with, in other words.

According to Carfagnini, “The Global Settlement was arguably the most significant milestone in the case. Given the number of jurisdictions involved and the various creditor and stakeholder interests, a global resolution was the only way the estates were going to be in a position to distribute money to creditors and pensioners in the various jurisdictions around the world. As you can imagine, the settlement itself was very complex, as it had to effectively shut the door on the myriad of issues that had arisen in the context of a multinational business and of its wind-down. In this regard, I would add that the work of retired Delaware Judge Joseph Farnan in mediating and facilitating the settlement at that critical time in the case was also important.”

D.J. Miller, a partner at Thornton Grout Finnigan LLP offers this explanation for why the decision made the deal: “The Global Settlement in Nortel announced on October 12, 2016, became somewhat inevitable after the Ontario Court of Appeal (OCA) issued 42-page written Reasons on May 3, 2016, dismissing an application by the bondholders and US debtor estate for leave to appeal the pro rata allocation decisions issued by the Canadian and US Courts. The very strong OCA decision led to the first level appeal court in Delaware, which had already heard the appeal but hadn’t issued a decision, referring the matter directly to the highest appeal court in Delaware for determination. Had a US Appeal Court reached a different conclusion than the OCA, it would have left the parties in limbo with no means to allocate the $7.3 billion in global proceeds and further costs being incurred, since any allocation required a consistent decision of the Canadian and US Courts. This would have been an ‘Armageddon’ scenario for creditors, who had already waited seven years with no distribution.

“The highest appeal court in Delaware had previously issued a harsh criticism over the costs incurred in the Nortel proceeding and the resulting impact on pensioners and other creditors. It therefore seemed unlikely that the same Court would overturn the underlying decision and go in a different direction than the OCA (which had already upheld the underling decision), as that would have sent the parties back to square one. At its simplest, once everyone came to that realization, it was just a matter of how much money would have to be transferred to bring it to an end. The contributors to, and beneficiaries of, the transfer of money following the allocation decisions were known from the outset, and never changed.”

Key Law Firms

Nortel Canada: Gowling WLG (Canada) LLP

Nortel Networks Inc.: Norton Rose Fulbright Canada LLP (Corporate/M&A, Restructuring, IP, Litigation); Torys LLP (Restructuring, Litigation)

Informal Nortel Noteholder Group: Bennett Jones LLP

US Official Committee of Unsecured Creditors: Cassels Brock & Blackwell LLP (Restructuring)

UK Pension Protection Fund and Nortel Networks UK Pension Trust Ltd.: Thornton Grout Finnigan LLP (Restructuring, Litigation); Blake, Cassels & Graydon LLP (Restructuring, Litigation)

Wilmington Trust, National Association: Dentons Canada LLP (Canadian Counsel)

Monitor, Ernst & Young: Goodmans LLP

Joint Administrators of Nortel Networks UK Ltd.: Davies Ward Phillips & Vineberg LLP; Lax O’Sullivan Lisus Gottlieb LLP

Former Directors and Officers of Nortel Canada: Osler, Hoskin & Harcourt LLP

Former employees and LTD beneficiaries of Nortel Canada: Koskie Minsky LLP

Ontario Superintendent of Financial Services: Paliare Roland Rosenberg Rothstein LLP

Morneau Shepell Ltd.: McCarthy Tétrault LLP

Nortel’s continuing Canadian employees: Nelligan O’Brien Payne LLP; Shibley Righton LLP

9. STELCO RESTRUCTURING

Another perennial favourite on Lexpert lists is the restructuring of Stelco Inc.. It had been operating under the protection of the Companies’ Creditors Arrangement Act (CCAA) since being granted an initial stay of proceedings in September of 2014. On June 9, 2017, the court approved its restructuring under the CCAA. On June 30, Bedrock Industries Group LLC announced that all of the closing conditions regarding its announced transaction had been satisfied and its acquisition of Stelco was closed.

Bedrock plans to continue steel operations, and approximately 2,200 existing jobs would continue at Stelco’s Hamilton and Lake Erie facilities. The Restructuring plan also has the necessary support from Stelco creditors, including the province, and Stelco employees. The company will now work with stakeholders to finalize the necessary supporting agreements. The restructuring plan is supported by a Memorandum of Understanding (MOU) between Bedrock and the Province of Ontario, which sets out a policy framework intended to protect jobs while allowing the continuation of pensions and other post-employment benefits (OPEBs). The MOU also protects the environment while providing the opportunity for Stelco’s lands to be used to create value for pensions and OPEBs.

McCarthy Tétrault LLP was counsel to Stelco. According to McCarthy’s James Gage, “The successful restructuring of Stelco was a significant achievement for the company and its key stakeholders, including its thousands of employees and retirees and the communities in which it operates, bringing closure to a lengthy and challenging CCAA process in a manner that preserved jobs, pensions and community interests. Stelco is now well positioned with its clean balance sheet and the energetic support of its new majority owner, Bedrock Industries, to take advantage of the many opportunities it has identified to grow its business and to assert itself as a leader in its markets.” Added Michael Amm of Torys LLP, counsel to a syndicate of underwriters led by Goldman Sachs and BMO Capital Markets: “The successful IPO demonstrated how an innovative restructuring transaction can transform an iconic company and return it to the public capital markets.”

According to the Province’s announcement: “This transaction would allow Stelco’s five pension plans — which are underfunded and would otherwise face wind-up at reduced benefits levels — to remain in place without reductions, providing benefits for service accrued prior to December 31, 2017. Pension coverage for service after 2017 would be addressed in separate agreements. The framework also includes provisions for the funding of the pension plans, subject to government approvals. The new company would make various lump sum and ongoing contributions, resulting in $430 million of new contributions to the pension plans over 20 years, $160 million of which is guaranteed directly by Bedrock.”

Key Law Firms

United States Steel: Wildeboer Dellelce LLP (Corporate, Tax); Thornton Grout Finnigan LLP (Restructuring, Litigation); Blake, Cassels & Graydon LLP (Restructuring, Litigation); Stikeman Elliott LLP (Restructuring, Pension)

Carnegie Pension Fund: Stikeman Elliott LLP

Bedrock Industries: Borden Ladner Gervais LLP (M&A and Corporate); Goldman Sloan Nash & Haber LLP (Restructuring)

Brookfield Capital Partners Ltd: Osler, Hoskin & Harcourt LLP

Wells Fargo: Norton Rose Fulbright Canada LLP (Pensions, Real Estate, Environmental, Tax, Competition, Employment)

IPO Underwriters: Torys LLP

Stelco Directors: WeirFoulds LLP

Monitor, Ernst & Young: Bennett Jones LLP

Salaried employees: Koskie Minsky LLP

USW Union: Davies Ward Phillips & Vineberg LLP (Co-Counsel)

USW Local Union 1005: Inch Hammond PC; Cavalluzzo LLP

Ontario Superintendent of Financial Services: Goodmans LLP (Restructuring, Corporate)

USW Union: Paliare Roland Rosenberg Rothstein LLP

SIDEBAR: Honourable Mentions

On an optimistic note, there were several more deals that drew praise and attention from the lawyers who weighed in on our top deals list. These too involved consolidation, and most notably, innovation.

10. PARKLAND FUEL ACQUIRES CHEVRON CANADA’S DOWNSTREAM FUEL BUSINESS

Closing the list of Top 10 on the consolidation theme, Chevron Corp., the second-largest US-based oil company, sold its Canadian gasoline stations and refinery in British Columbia to Parkland Fuel Corp., a marketer of petroleum products, for $1.46 billion. In a Reuters report, Parkland CEO Bob Espey said, “The acquisition adds scale to Parkland and gives the company significant supply infrastructure and logistics capability to support Parkland’s existing operations.” The assets include 129 gasoline stations, three terminals and the Burnaby oil refinery, located east of Vancouver. The refinery can process 52,000 barrels of oil a day.

Sven Milelli, leading McCarthy Tétrault LLP’s M&A team for Parkland wrote, “This was a transformational deal that cements Parkland’s status as Canada’s leading fuel retailer while strategically expanding its supply infrastructure with the acquisition of the iconic Burnaby Refinery and related marine terminals.”

Key Law Firms

Parkland: Bennett Jones LLP (Competition); McCarthy Tétrault LLP (Corporate, Labour & Employment, and Pensions, Litigation, Real Property, Environmental, Tax); Paul, Weiss, Rifkind, Wharton & Garrison LLP; Dorsey & Whitney LLP (US Antitrust)

Chevron: Osler, Hoskin & Harcourt LLP

Underwriters: Dentons Canada LLP