(Photo: Ashley White (Bennett Jones), Jason Bullen (Cassels Brock & Blackwell ), J.R. Laffin (Stikeman Elliott), Tim McCormick (Borden Ladner Gervais))

If there ever were a year in M&A activity that you could call schizophrenic, it would probably be 2022. It started in high gear, coming off a phenomenal 2021, then slowed considerably in the second half.

The big question, however, is what sort of year for M&A will 2023 bring.

“What’s the new normal in M&A? That’s a good question,” says Tim McCormick, partner with the national corporate and capital markets group at Borden Ladner Gervais LLP. Thanks to the pent-up demand brought on by the COVID-19 pandemic that made 2021 such a big year for M&A, McCormick says any subsequent year would have to meet a very high bar.

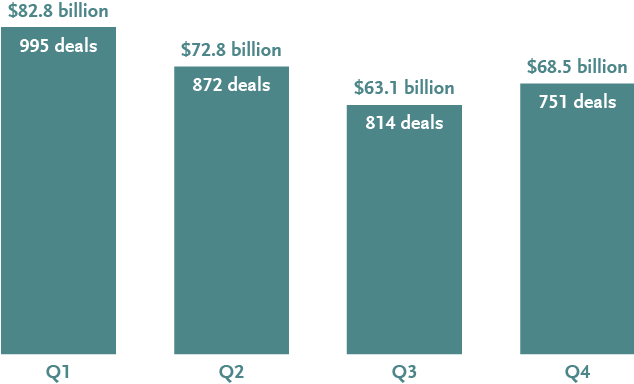

A January report by Bennett Jones LLP notes there were over 3,400 deals in Canada in 2022, with a combined volume of nearly US$290 billion. The first half of the year was significantly stronger in deal volume than the second half – US$155.6 billion versus US$131.6 billion. However, the total value of deals picked up in the fourth quarter. Interestingly, November was the busiest month in M&A volume in 2022, but it was preceded and followed by the least active months – October and December.

“It was a bit frenetic in 2022,” says Ashley White, partner and co-head of Bennett Jones’ energy practice and one of the report’s authors. “There were downtimes; there were times of activity and opportunity for those ready to capitalize on those opportunities.”

J.R. Laffin with Stikeman Elliott LLP describes 2022 as a tale of two markets for mergers and acquisitions. He says inflation, higher interest rates, and the possibility of a recession fuel uncertainty. There was also Russia’s invasion of Ukraine and other geopolitical issues like squeezed or shifting supply chains and capacity issues.

“It was no longer the frenzy of ‘grow at all costs’ that was driving M&A,” Laffin adds. And while there is still a lot of “dry powder” out there for transactions, especially private equity, those with the money are now pickier about the metrics needed to make a good acquisition.

Some strategic buyers also decided to take a breather on M&A and either conserve cash or address debt, with concerns about getting access to capital as banks slow down the cash flow. Banks aren’t writing as many sizeable loans as they had been doing previously.

But Laffin points out that it’s not all gloom and doom for M&A in 2023. And it certainly isn’t as tough in M&A as it is for those working in initial public offerings, which have seen a considerable plunge in activity.

“There is still a lot of kicking of the tires,” he says, pointing out that buyers are doing their homework and getting ready to pounce as they wait for sellers who were expecting higher valuations to re-evaluate their lofty aspirations.

He adds: “Are there going to be massive blockbuster deals where we see huge premiums paid? Probably not. But there are going to be smart deals, and people will figure out a way to get them done.”

McCormick agrees that there are deals to be done. But he adds there will likely be “more complexity in the deals that do happen, simply to address the fact that markets are tighter.”

One example he points to is Yamana Gold’s assets being split between Pan-American Silver taking the company’s Latin American resources and Agnico Eagle Mines taking Yamana’s Canadian assets.

These include Yamana’s portion of the Canadian Malarctic mine in northwestern Quebec, which Agnico Eagle has shared with Yamana since 2014.

McCormick says, “It made more sense to the company to extract higher value by splitting up the assets. And that makes for more complex transactions, as more parties are involved.”

McCormick says deals may also become more complex as the regulatory regime becomes stricter, especially in the resource space, particularly critical minerals such as lithium.

“That is certainly going to weigh heavily in 2023 in terms of sources of capital, whether it’s in the critical mineral space, artificial intelligence, or any sort of research and development on the tech side that our Canadian government has funded.”

Laffin agrees that more concerns about foreign investors and national security will have an impact on dealmaking if for no other reason than narrowing the field of potential buyers. “It might be as simple as certain foreign investors self-selecting not to put themselves in the running,” he says, if, for example, state-owned enterprises of countries such as China run the risk of having their deal rejected.

Another theme for 2023 that McCormick sees playing out is more shareholder activism. “I think we’re going to see activist investors taking more of a role in unlocking value at the company level or forcing change,” he says. “And I think boards and management teams need to be prepared to readjust their valuations with that in mind. Or else they will see pressure from shareholders to unlock value,” he says, either from a sale of non-core assets or the whole company itself, “according to the fiduciary duty management and boards must adhere to.”

Adds McCormick: “I think a lot of companies don’t yet realize they are going to be a target and that they may have to adjust their expectations to what the buyers are willing to pay.”

The Bennett Jones report notes that shareholder activist campaigns increased in the second half of 2022 despite an overall decline year over year. As well, shareholder proposals more than doubled from 2021 to 2022, “suggesting a potential for more activism in 2023 as dealmakers seek alternative means of unlocking value.”

Laffin points out that acquisition through insolvency may become more of a factor in 2023. At the pandemic’s start, “there was a lot of government assistance and a willingness among lenders and suppliers to be lenient on those owing money.” This kept many companies out of insolvency.

However, as the worst of the pandemic’s impact is now over, along with rising interest rates and less government support, Laffin says, “more companies will be staring down the path of insolvency.”

Buying a company out of insolvency hearings can be a “pretty clean” process, Laffin notes, because the court monitors the proceedings, so buyers generally “know what they are getting.” Even the pre-insolvency period can be a good time for buyers “since they obviously have a lot of leverage” when a company faces bankruptcy.

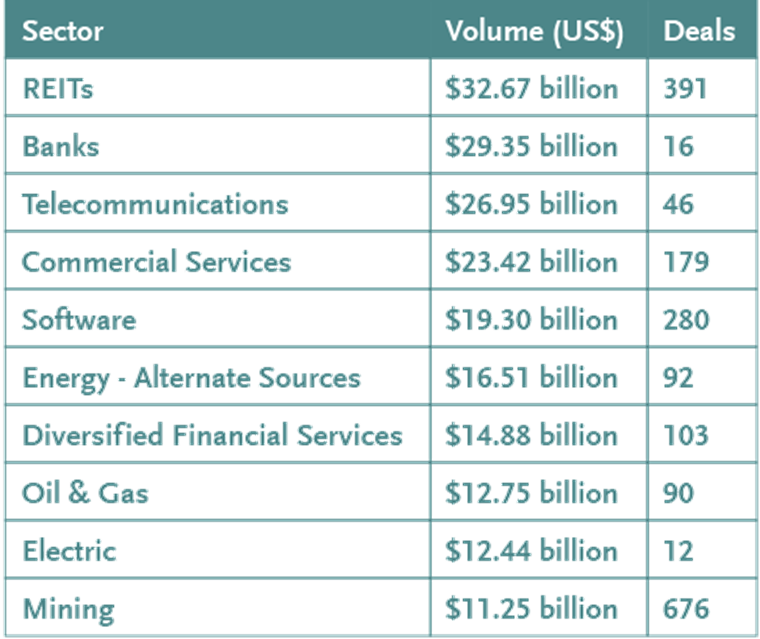

A look at 2022 dealmaking from a sector perspective could also hold some clues for the current year. The Bennett Jones report says REITS led the way in Canadian M&A volume by sector with US$32.67 billion in deals.

Banks were next, with some of the largest deals of 2022. The banking and diversified financial services sectors accounted for US$44.23 billion in activity combined – one of the busiest years for M&A activity in the Canadian financial services sector in recent memory.

The software sector was in fifth place, dominated by $13 billion in applications software and US$5.7 billion in enterprise software. There was more volume in alternate energy sources than in oil & gas – taken together, the sectors totalled US$29.26 billion in deals. Mining saw over $11 billion in volume, with the highest deal count in 2022.

Although pressures will remain in 2023, the Bennett Jones report says M&A activity will be positive, with some impressive activity in sectors such as technology and software, battery metals in the mining sector, healthcare, and agribusiness. Given that Canada’s energy transformation is relatively early, areas such as biofuels, hydrogen, and carbon capture, utilization, and storage are also well-situated to attract investor interest.

White at Bennett Jones says investors will be looking at balancing risks in the short term with long-term strategies. White works mostly in energy and alternative energy, where she sees the traditional oil and gas space focusing on core assets, though perhaps “using a sharper pencil.” She also sees more pursuit of partnerships and joint ventures to build competitive advantage.

As for the mid-market space, in the $50 million to $400 million range, Jake Bullen, co-chair of the private equity group at Cassels Brock & Blackwell, says he sees M&A activity staying “robust” compared to “mega deals.” He predicts the valuation gap between buyers and sellers will narrow as both sides process information about the market and the economy. And their smaller size means they will be easier to complete.

And while there will likely be a decrease overall in dealmaking, thanks to economic considerations such as higher interest rates and geopolitical risk, these factors will probably have less impact on the mid-market.

“Unlike megadeals, there’s less sensitivity to interest rates in the mid-market,” says Bullen. “And a private equity fund or a strategic buyer may finance more of it from cash on hand, or shorter-term loans,” making them less sensitive to interest rate increases.

Learn how to start a private equity fund in Canada in this article.

The second reason Bullen cites for maintaining an optimistic view is that “there is a lot of money out there to be put to work” in the mid-market. While it may take a little longer to get the target return on investment, Bullen says, “if there is a good deal to be done, and if the numbers make sense, you’ll do the deal.”

Laffin says he is still “giving a lot of upfront advice to clients.” Potential buyers are doing a lot more initial planning.

“It’s more cautious, and [there is] more thought about when to take advantage of opportunity. Then they move just as quickly when the time is right.”

As for McCormick, he says he likes to think boards “will start to reassess the valuations they are looking for,” either because they’ll accept reality or are financially strapped and need to do so. “That, combined with shareholder activism, will encourage more transactions.

“I think 2023 will be a fascinating year for M&A. We may not see 2021 again for a while, and there will be all sorts of pressures, but people want to do deals, and there are deals to be done. I’m excited about it.”

| 2023 M&A OPPORTUNITIES IN CANADA BY SECTOR |

|---|

|

| 2023 TRENDS TO WATCH IN CANADA |

|---|

|

2022 CANADIAN M&A ACTIVITY, BY QUARTER

SOURCE: Bennett Jones, Bloomberg

2022 CANADIAN M&A ACTIVITY, BY SECTOR

SOURCE: Bennett Jones, Bloomberg