In a world where large-scale infrastructure projects can take decades from development to completion, the political machinations of a particular point in time – including the current possibility of a full-scale trade war with the United States – are often just a blip on a calendar with a protracted timeframe.

So yes, we may see disruption in decades of trade pattern norms under free trade agreements such as the Canadian-United States-Mexico Free Trade Agreement (CUSMA). This may also have some impact, at least in the short term, on infrastructure projects and the dealmaking that goes with such ventures. However, lawyers working in infrastructure and energy project development, financing, mergers, and acquisitions say that, ultimately, these projects will still be needed, financed, and bought and sold when necessary.

Says Thomas J. Timmins, who leads Gowling WLG’s energy practice in Canada: “These projects have a long gestation period, a long construction phase and are long-lived once built…In the current political climate between the United States and Canada, this is likely just a blip.” From the perspective of project developers, he says, “What they are looking for are large-scale mega trends and how we’ll meet our future needs through the development of projects such as public transportation, pipelines, data centres and solar energy, to name just a few.”

That’s not to say there won’t be some disruption regarding M&A and dealmaking in infrastructure.

Timmins’ colleague Peter Bouzalas notes that “upstream” infrastructure projects will most likely be most impacted.

“Interest rates and tariffs can impact those transactions, and they can slow them down if there is volatility or uncertainty,” he says. “Once there is stability, even if it differs from before, things start to pick up again.

“Right now, I’m seeing a lot of ‘wait and see’ associated with tariffs.” And given the significant recent fluctuations in this US administration’s approach to imposing tariffs, it may take some time for the dust to settle.

Matthew Bernado, another partner in Gowling’s infrastructure and construction industry group, says there are different ways for public authorities to fill an infrastructure gap. They range from traditional procurements or more progressive delivery models, where the public authority will ultimately own and operate the infrastructure after it is built, to public-private partnerships (P3s) where private sector consortia come together to build, finance, and then operate and maintain a project for a specified concession granted by the public authority. This creates an asset that brings in long-term cash flow. Examples include a pipeline, energy grid or toll highway.

“Putting these projects together isn’t M&A in the traditional sense,” he says, though ownership in these projects can be later bought and sold once the project has been significantly de-risked.

For example, the 407 ETR, which is operated privately under a 99-year concession and ground lease agreement signed with the Ontario government, was sold in 1999 for about $3.1 billion to a consortium of Canadian and Spanish investors. The Canada Pension Plan Investment Board has since acquired a majority stake in the highway through a series of transactions, and one of the original owners, AtkinsRéalis (previously SNC Lavalin), has gradually sold its stake in the project, the last of which implied a value of over $40 billion for the highway.

Bernado notes that getting such projects off the ground can be challenging when tariffs and material costs are uncertain. This may result in some projects being temporarily put on hold until costs and risks can be analyzed.

Tariffs “may mean more money to build a project, and either the government, the private sector or the end user, or some combination of all of them will have to deal with that risk,” Bernardo says. “But there are contractual and policy arrows in our quiver to deal with this sort of challenge, so it doesn’t mean we have to throw up our hands and say we can’t do it.”

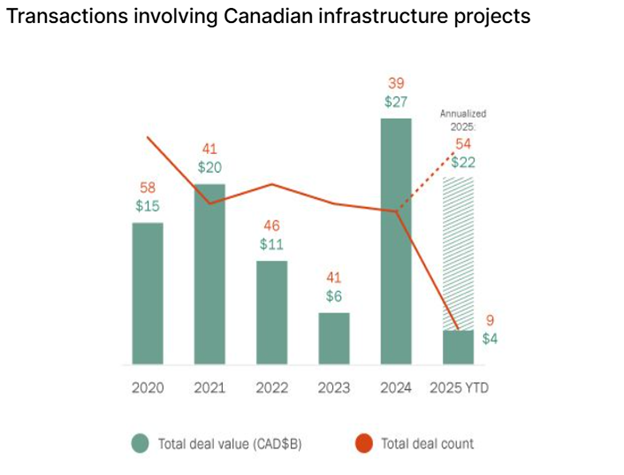

In a recent note, Huw Evans and Krista Hill at Torys LLP wrote that M&A activity in Canadian infrastructure was strong, with 39 deals in 2024 totalling $27 billion.

They added that, with nine deals already completed in the first two months of the year, the trend for 2025 looks promising. If the pace continues, there will be more than 50 transactions worth about $22 billion.

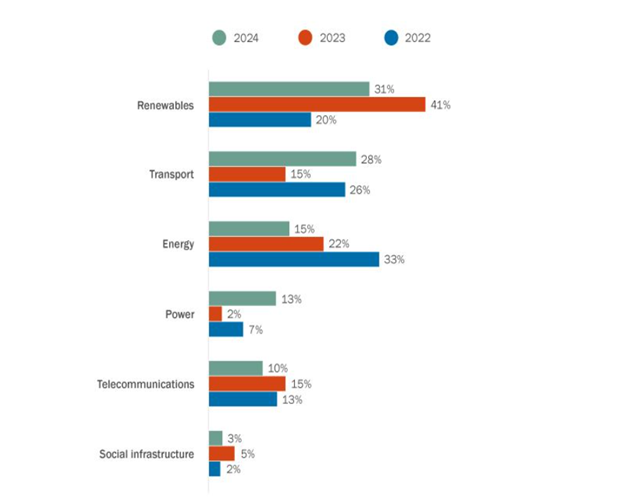

Renewable deals led the infrastructure M&A space in 2024, accounting for 31 percent of the total. The trend continued in early 2025, with deals such as Sitka Power Inc.'s acquisition of a portfolio of operating renewable electricity generation and battery energy storage assets from Saturn Power Inc. and Connor, Clark & Lunn Infrastructure's acquisition of an interest in the 180 MW Armow Wind and 149 MW Grand Renewable Wind projects in southern Ontario from Pattern Energy Group LP.

However, Evans and Hill point out that US tariffs on Canadian energy and other goods and proposed retaliatory tariffs are “clouding deal forecasting” as dealmakers seek to shield themselves from a market turndown.

Furthermore, they say, recent investment policies from both countries – the US's "America First" investment policy and Canada's stricter foreign investment review policy – could impact transactions.

Geoffrey Stenger, head of the infrastructure industry team at Bennett Jones LLP, agrees that those who want to get involved in infrastructure M&A will be looking for “certainty on the nature of returns on the asset in Canada vs. other jurisdictions, in the sense of understanding any tariffs involved, end market for what is produced by the asset, perhaps preferring a local customer base not subject to tariffs, the regulatory environment, and what inflation protection any asset can offer.”

He notes that M&A in oil – and gas-related infrastructure could pick up, especially as US tariff fears expand oil, gas, or LNG production in Canada, including contemplated projects in a west-east direction rather than north-south direction. That could also lead to increased infrastructure M&A activity.

“We’re reasonably bullish on the infrastructure space this year – there’s lots in the hopper – but with all the global uncertainty, do we know exactly what the landscape will look like? I don’t think anyone knows, but the negative sentiment is not yet showing up in the data or in our activity levels.”

Data centre infrastructure is another area of significant growth.

Such centres are filled with computer servers used by companies like Meta, the owner of Facebook and Instagram, to develop and train large-scale artificial intelligence models.

A recent report by the Independent Electricity System Operator (IESO) indicates that growth in Canadian data centre projects has increased the electricity demand forecast, and significant deal activity in the energy sector is already underway to support the proliferation of data centres.

Investment activity in this space includes Equinix's $15B joint venture with GIC and Canada Pension Plan Investment Board for xScale data centre portfolio development and an announcement that Pembina Pipeline Corp. is investing in a large natural gas power plant that could supply a massive data centre complex.

Ontario's Hydro One has four major transmission projects planned and recently completed the acquisition of a 48 percent interest in the East-West Tie Limited Partnership from affiliates of OMERS Infrastructure Management Inc. and Enbridge Transmission Holdings Inc. The East-West Tie Limited Partnership owns a 450-kilometre, 230kV double-circuit transmission line regulated by the Ontario Energy Board.

In September 2024, Axium Infrastructure announced that one of its funds acquired an 80 percent equity interest in PUC Transmission LP, a regulated transmission utility established to construct and operate a greenfield transformation station and transmission line in Sault Ste. Marie, Ontario. The project will power, among other connections, Algoma Steel Inc.'s transition to using electric arc furnaces to reduce CO2 emissions.

In the so-called “secondary” market for dealmaking in the infrastructure sector, equity owners look to buy and sell interests in a project after it is completed or significantly de-risked. Sarah Bird, partner with the infrastructure practice at Borden Ladner Gervais LLP in Vancouver, says it is fair to say that the deal flow in this market has been impacted recently by the uncertainty in the economy.

“Still, we hear lots of interest from our clients who are considering buying or selling operational projects in Canada. So, despite some of the uncertainty, I think there is still an appetite to look at opportunities in the Canadian secondary market for infrastructure projects."

She also notes, "It will be interesting to see if some of our large infrastructure players in Canada will be seeking out more opportunities to focus on Canadian infrastructure projects when they might otherwise have been looking for such projects in other jurisdictions.”

Bird also says there appears to be growing interest in developing interprovincial projects, removing barriers between provinces, and building essential infrastructure in areas such as critical minerals, public infrastructure, and energy. With the input of government money – especially if infrastructure is seen as a tool to keep the economy going if we enter a recession – such projects may be developed more.

Indeed, Bird’s colleague Doug Sanders says that while there is still a lack of clarity on the economy's future, “two categories of infrastructure projects seem to be developing now.”

One category is projects that are needed “irrespective of what is happening south of the border.” The other category includes projects that have been significantly advanced in timing, or where there is a renewed interest in projects that had been put on the back burner.

For example, in British Columbia, Sanders says 18 significant infrastructure projects have been moved forward, ranging from mining to energy and LNG, and many are “projects aimed at creating less reliance on the United States.

“Some of these projects are new, some have been fast-tracked, and some were shelved for political reasons but have now been brought back for reconsideration.”

It’s a mixture of all these things, but it leads to a pretty robust infrastructure market.”

Sectors include energy, renewables, social infrastructure, telecommunications, transport, and power. Excludes cancelled deals.

Canadian infrastructure deal activity by industry