For decades, the initial public offering occupied a privileged place in corporate finance. It represented the natural evolution of a successful private company and the principal gateway to large-scale growth capital. In Canada, public markets played a particularly important role in financing emerging businesses, especially in the resource, technology and life sciences sectors.

That model has come under increasing pressure.

Between 2022 and 2025, Canadian IPO activity declined dramatically. Rising interest rates, inflationary pressures, geopolitical instability and market volatility contributed to a significant reduction in public offerings. Many private companies elected to postpone public listings, while others sought capital through private equity, venture capital, sovereign wealth funds or strategic investors. The resulting decline prompted broader questions about the future of Canada’s public markets. Were the challenges facing IPOs merely cyclical, or were they indicative of a more permanent shift in how companies finance growth?

By 2026, however, conditions began to improve. Public equity markets strengthened, investor confidence returned and several high-profile offerings demonstrated a renewed appetite for new public securities. At the same time, a growing number of Canadian and international issuers began evaluating Canadian markets alongside American stock exchanges, creating a competitive dynamic that would have been less pronounced a decade earlier.

The proper lens through which to view the recent Canadian IPO market is not recovery, but restructuring. The Canadian public markets remain highly relevant, particularly in sectors such as mining and critical minerals. However, the rationale for becoming a public company, the legal obligations associated with public-company status and the competitive alternatives available to private companies have fundamentally changed.

For boards and management teams, the decision to pursue an IPO has become as much a governance and legal decision as a financing decision.

The state of the Canadian IPO market in 2026

The first half of 2026 marked the strongest period for Canadian IPO activity since the post-pandemic boom years.

The successful IPO of Apotex Health Corp. (TSX: APTX) represented the largest Canadian public offering in approximately five years and signaled renewed institutional confidence in quality issuers with established operating histories. More broadly, market participants reported a substantial increase in issuer inquiries and listing preparations.

The improvement reflects several factors. Inflationary concerns that dominated markets in 2022 and 2023 have largely subsided. Interest rates appear to have stabilized, reducing uncertainty around valuation models and capital costs.

Public equity markets have recovered significantly. Strong commodity prices, resilient financial institutions and improving economic sentiment have supported Canadian equity performance.

Investors appear increasingly willing to finance businesses associated with several dominant investment themes, including artificial intelligence, energy security, electrification, infrastructure development and critical minerals.

Yet despite these positive developments, the Canadian IPO market remains materially different from prior cycles. Historically, public markets represented the principal source of growth capital for scaling companies. Today, public markets compete directly with private capital providers possessing unprecedented financial resources. Large institutional investors that previously participated almost exclusively in public markets now routinely invest in private companies.

As a result, companies are remaining private longer and entering public markets later in their development cycle. The average IPO candidate in 2026 is generally larger, more mature and more operationally sophisticated than its counterpart a decade earlier.

The consequence is a market characterized by fewer but larger offerings.

The enduring value of the long-form IPO

The renewed interest in traditional IPOs should also be understood against the backdrop of the alternative listing structures that proliferated during the exceptionally accommodative capital markets of 2020 and 2021. Reverse takeovers ("RTOs"), qualifying transactions involving capital pool companies, and, particularly in the United States, special purpose acquisition companies ("SPACs"), offered private companies an expedited path to the public markets at a time when capital was abundant and investor appetite appeared insatiable. In many cases, these go-public structures served legitimate commercial purposes and provided an efficient route to both capital and liquidity. However, the subsequent performance of a significant number of de-SPAC transactions and certain speculative RTO issuers materially altered investor sentiment. As valuations contracted and many newly public companies failed to achieve their business plans or projected financial performance, institutional investors became increasingly skeptical of transactions perceived to have reached the public markets without the rigorous scrutiny traditionally associated with a fully marketed IPO.

This shift in investor psychology has had important implications for Canadian issuers. Although Canadian securities law affords multiple pathways to becoming a reporting issuer, the long-form IPO continues to occupy a unique position within the market. Unlike an RTO or other alternative listing transaction, a conventional IPO requires the preparation of a comprehensive prospectus, extensive legal and financial due diligence, detailed regulatory review, institutional marketing through a roadshow, and the reputational endorsement of established underwriters willing to place their balance sheets and credibility behind the offering. Collectively, these elements perform a valuable signalling function. They provide prospective investors with confidence that the issuer has been subjected to extensive scrutiny by sophisticated market participants before the issuer’s securities are broadly and publicly distributed.

For many of Canada's leading institutional investors, this distinction remains significant. While investment decisions ultimately depend upon the quality of the issuer rather than the mechanics of its listing, a long-form IPO frequently serves as an important indicator of governance maturity, disclosure discipline and management preparedness. Institutions that are expected to deploy substantial amounts of long-term capital often view the IPO process itself as evidence that an issuer has successfully navigated the demanding legal, accounting and governance standards expected of public companies. By contrast, issuers that access the market through alternative listing structures may find that they must earn this credibility over time through operational execution and sustained disclosure performance rather than inheriting it at the time of listing.

Accordingly, the renewed prominence of the long-form IPO in 2026 should not be viewed merely as a matter of regulatory procedure. Rather, it reflects a broader market preference for rigorous diligence, transparent disclosure and institutional-quality governance after a period in which speed to market frequently appeared to take priority over public-company readiness. In a market increasingly defined by selectivity rather than speculation, the long-form IPO has re-emerged as the benchmark against which new public issuers are measured.

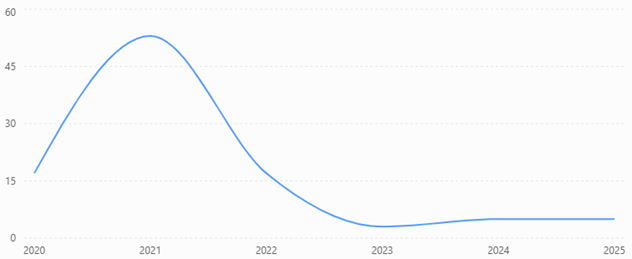

Data from the TMX Group supports the notion that 2021 was the peak “everything can go public” year; 2022 – 2024 were a reset; 2025 showed renewed financing strength, but only with five true-operating-company IPOs across the TSX/TSXV; and 2026 is showing activity, but much of the headline new-listing volume is still ETFs rather than traditional-issuer IPOs.

TMX’s data shows 449 new listings in 2021, including 237 companies, 88 CPCs and 4 SPACs; by 2022, total new listings fell to 274 and operating-company IPOs dropped from 53 to 17. The trough became more pronounced in 2023: only 3 operating-company IPOs across TSX/TSXV, despite 221 total new listings.

Figure 1. Traditional Operating-Company IPOs on the TSX and TSX Venture Exchange (2020–2025)

Mining remains the counterweight. The TMX reported 54 new listings in the mining sector in 2025, and the mining sector totalled 1,073 issuers across TSX/TSXV in 2025, with more than C$1.1 trillion in aggregate market capitalization for the mining sector. The TMX reported that C$16 billion in mining equity capital was raised by its listed issuers in 2025.

Mining remains Canada’s comparative advantage

While many sectors have experienced profound change, mining remains Canada’s most durable public market strength.

Canada continues to occupy a unique position within global resource finance. The Toronto Stock Exchange and TSX Venture Exchange collectively support one of the world’s most sophisticated mining finance ecosystems. Investors, regulators, analysts, lawyers, accountants and technical consultants possess extensive experience evaluating everything from upstart mineral exploration and development projects to long-producing mining companies.

This ecosystem creates meaningful advantages for mining issuers.

Unlike many industries, mining companies often require investors to evaluate complex technical information long before meaningful revenues are generated. Mineral-resource estimates, metallurgical studies, permitting pathways and development timelines frequently matter more than historical financial performance.

Canadian markets have developed specialized mechanisms to accommodate these realities. National Instrument 43-101 provides a “best-in-class” comprehensive disclosure framework governing scientific and technical information, while institutional investors possess decades of experience evaluating exploration and development-stage projects.

These advantages remain substantial. As a result of providing knowledgeable and experienced investors with timely, high-quality, reliable and fulsome disclosure, issuers are able to obtain cost-of-capital and valuation advantages.

Yet a notable development has emerged in recent years. Although Canada continues to dominate early-stage mining finance, larger mining companies increasingly consider American stock exchanges as their primary public market destination. This trend raises important questions regarding the future competitiveness of Canadian capital markets.

Canada or the United States? Comparing the TSX and NASDAQ/NYSE for mining IPOS

For mining issuers, listing venue has become one of the most consequential strategic decisions confronting management and boards.

Historically, Canadian mining companies overwhelmingly listed in Canada. Today, that assumption no longer holds.

1. The Canadian advantage

Canada’s principal advantage is expertise.

Canadian investors understand exploration risk. They understand resource estimates, feasibility studies, streaming arrangements and project development timelines. They understand that value creation in mining frequently occurs long before production begins.

The TSX Venture Exchange in particular remains unmatched as a financing platform for exploration-stage companies.

Canada also offers a regulatory framework specifically designed for mining issuers. National Instrument 43-101 provides certainty regarding technical disclosure obligations and establishes clear standards governing mineral resource and reserve reporting.

For exploration and development-stage issuers, these advantages remain compelling.

2. Execution efficiency and transaction costs

Beyond sector expertise and regulatory familiarity, Canada offers a practical advantage that is often underappreciated by boards considering where to undertake an IPO: execution speed.

A conventional Canadian IPO can be completed within approximately three to four months from organizational meeting to closing, assuming the issuer is otherwise public-company ready. By contrast, a comparable U.S. IPO commonly requires six months or longer, reflecting the SEC registration statement review process, multiple rounds of staff comments, and the generally more extensive disclosure and diligence process associated with U.S. securities offerings. Although timing necessarily depends upon the complexity of the issuer, the quality of its disclosure and prevailing regulatory workloads, the Canadian process is, in most cases, materially shorter.

This difference has strategic significance beyond simple convenience. Equity capital markets are inherently cyclical, and investor sentiment can change rapidly in response to macroeconomic developments, commodity prices, interest rates or geopolitical events. A compressed execution timeline reduces market risk by allowing issuers to capitalize more quickly on favourable market windows. Conversely, a transaction that remains exposed to market conditions for six months or longer faces a materially greater risk that adverse developments will require repricing, restructuring or even withdrawal of the offering. In this respect, Canada's more streamlined IPO process may provide issuers with a meaningful competitive advantage in volatile markets.

The shorter timetable also translates into lower transaction costs. Because Canadian prospectus offerings generally involve a less protracted regulatory review and do not typically require the extensive Rule 10b-5 negative assurance practice that has become a standard feature of U.S. registered offerings, legal fees are often materially lower than those associated with a comparable U.S. IPO. Accounting costs, management time and overall transaction expenses likewise tend to be reduced by virtue of the shorter execution period. For emerging growth companies and development-stage mining issuers, these savings can represent a meaningful percentage of the total cost of accessing the public markets.

3. The Canadian limitation

Canada’s principal limitation is scale.

The pool of available institutional capital remains smaller than that available in the United States. Trading liquidity is often lower, analyst coverage can be more limited and for valuation multiples may be constrained by the size of the domestic market.

These limitations become increasingly important as projects grow and companies mature.

A company seeking hundreds of millions—or billions—of dollars to construct a major mine may require access to larger pools of institutional capital than Canadian markets can efficiently provide.

4. The U.S. advantage

American stock exchanges offer significant benefits.

The NYSE and Nasdaq provide access to deeper capital markets, broader institutional participation and larger trading volumes. U.S. investors have demonstrated increasing interest in mining companies connected to critical minerals, copper, uranium and energy transition themes.

For large-scale projects, a U.S. listing can increase visibility among generalist investors, sovereign wealth funds and strategic industrial investors.

The result may be improved liquidity, stronger valuations and enhanced financing flexibility.

5. The U.S. cost

These benefits are accompanied by meaningful legal burdens.

American issuers face greater exposure to securities litigation, more extensive regulatory compliance obligations and heightened disclosure scrutiny.

Public-company governance expectations are also generally more demanding. Compliance costs associated with SEC reporting, internal controls and Sarbanes-Oxley obligations can be substantial.

For many issuers, the question is not whether a U.S. listing offers advantages, but whether those advantages justify the additional costs and risks.

6. The emerging dual-listing model

An increasingly common approach involves a staged market strategy where a company will establish an initial public market presence in Canada and then subsequently pursue a U.S. listing as projects mature and capital requirements expand.

A common first-stage approach is to be listed on the TSX/TSXV in Canada and also have the company’s shares trade on the OTCQX in the United States (which is U.S. securities marketplace, but not a stock exchange with traditional listing requirements or where the issuer must have SEC registration). This approach leverages Canada’s strengths while preserving access to deeper U.S. capital pools. In the second stage, the company would remain on the TSX/TSXV; however, it would also become listed on the NYSE or Nasdaq stock exchanges, which would typically become the company’s primary exchange in terms of trading volume.

However, dual listings create additional governance, compliance and reporting burdens. They should be pursued only where clear strategic benefits exist.

The new IPO readiness paradigm

The traditional conception of IPO readiness focused heavily on financial reporting. That approach is no longer sufficient. Modern IPO readiness encompasses governance readiness, disclosure readiness and cultural readiness.

1. Governance readiness

Institutional investors increasingly evaluate governance before evaluating valuation.

Companies contemplating an IPO should establish:

- Independent boards;

- Effective audit committees;

- Formal risk oversight frameworks;

- Appropriate executive compensation structures;

- Succession planning mechanisms; and

- Robust governance policies.

Public market investors increasingly treat governance quality as a proxy for management quality.

2. Disclosure readiness

Disclosure obligations have expanded significantly. Boards must evaluate risks relating to:

- Cybersecurity;

- Artificial intelligence;

- Geopolitical instability;

- Climate change;

- Supply chains;

- Indigenous relations;

- Human capital management; and

- Data governance.

Mining issuers face additional obligations concerning technical disclosure and qualified person oversight.

3. Cultural readiness

The most overlooked component of IPO readiness is cultural readiness. A private company operates differently from a public company. Management must adapt to continuous disclosure obligations, investor scrutiny, analyst engagement and quarterly reporting cycles. Failure to appreciate these significant changes remains a common cause of post-IPO underperformance.

Fiduciary duties and board oversight during the IPO process

The board’s role during an IPO extends well beyond approving a prospectus. Directors owe fiduciary duties to the corporation and must exercise their responsibilities with diligence and care throughout the offering process.

Particular attention should be paid to:

- Prospectus disclosure;

- Risk factor development;

- Related-party transactions;

- Executive compensation;

- Underwriting arrangements;

- Corporate governance structures; and

- Long-term strategic implications of becoming public.

In many respects, the IPO process serves as a governance stress test. Weaknesses that remain hidden in private companies frequently become visible during public market scrutiny.

Liability considerations

The legal consequences of inadequate disclosure have become increasingly significant.

Directors, officers, underwriters, auditors and experts may all face liability for material misrepresentations contained within prospectus disclosure.

The growth of securities class actions further increases these risks. Accordingly, due diligence should not be viewed as a procedural exercise. It remains the primary mechanism through which participants establish and preserve available legal defenses.

Particular care should be exercised when preparing any:

- Forward-looking information;

- Mineral resource and reserve estimates;

- ESG disclosures;

- Emerging-market disclosures;

- AI-related disclosures; and

- Cybersecurity disclosures.

These areas represent increasing sources of regulatory and litigation risk.

The future of Canadian public markets

The evidence suggests that the Canadian IPO market is recovering. However, recovery should not be confused with restoration.

The public markets of 2026 differ fundamentally from those of previous decades. Private capital now competes directly with public markets. U.S. exchanges compete directly with Canadian exchanges. Institutional investors demand higher standards of governance and disclosure. Public-company obligations continue to expand.

These developments are unlikely to reverse. Accordingly, the future Canadian IPO market will likely feature:

- Fewer but larger offerings;

- Greater concentration in mining and critical minerals;

- Stronger governance expectations;

- More sophisticated disclosure practices; and

- Increased competition with American stock exchanges.

Canada retains substantial strengths, particularly in mining finance. Whether those strengths remain sufficient to attract the next generation of large-scale issuers remains one of the defining questions for Canadian capital markets policy.

Adapting to the next era

The central question confronting Canadian capital markets in 2026 is not whether IPO activity will return. It has already begun to return.

The more important question is whether Canadian markets can remain competitive in an environment where private capital and U.S. stock exchanges offer increasingly attractive alternatives.

For private companies, the lesson is clear. An IPO is no longer merely a financing transaction. It is a strategic transformation that reshapes governance structures, disclosure obligations, investor relationships and corporate culture.

The most successful issuers will not necessarily be those that identify the perfect market window. Rather, they will be those that approach public-company readiness as a comprehensive legal, governance and strategic undertaking.

Viewed through this lens, the Canadian IPO market of 2026 is best understood not as a market recovering from temporary weakness, but as a market adapting to a fundamentally different capital-formation environment. The companies that recognize this transformation will be best positioned to succeed in the next era of Canadian public markets.

***

Andrew Powers co-leads the firm’s Mining Law Group and is a partner in the firm’s Business Law Group in Toronto. Recognized as a leader in his field, Andrew’s practice focuses on corporate and securities law, including corporate finance, mergers and acquisitions, corporate governance and shareholder activism.

Geoff Clarke co-leads the Mining Law practice at the firm, focusing on corporate, securities and capital markets matters. He offers practical solutions to leading companies, global businesses, institutional investors and investment banks, focusing on securities offerings, mergers and acquisitions, corporate governance, shareholder activism, fairness opinions and continuous disclosure. With experience in mining and financial services, Geoff’s advice is valued for its business acumen. Geoff is currently the Lead Instructor for the Corporate Finance course at the University of Windsor Law School, which is a course he has taught since September 2007.