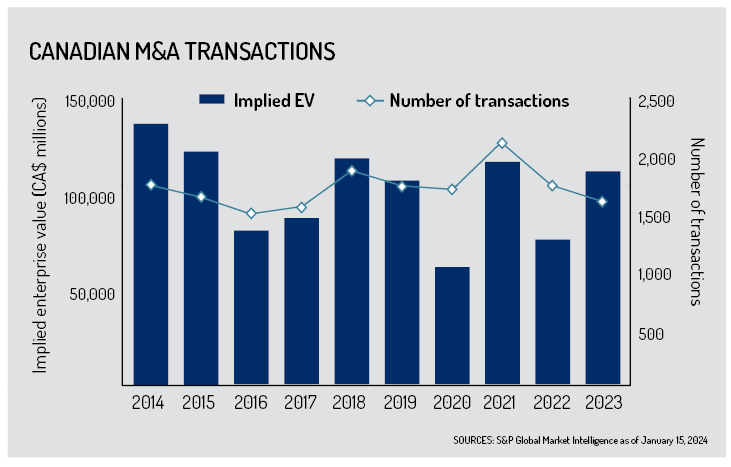

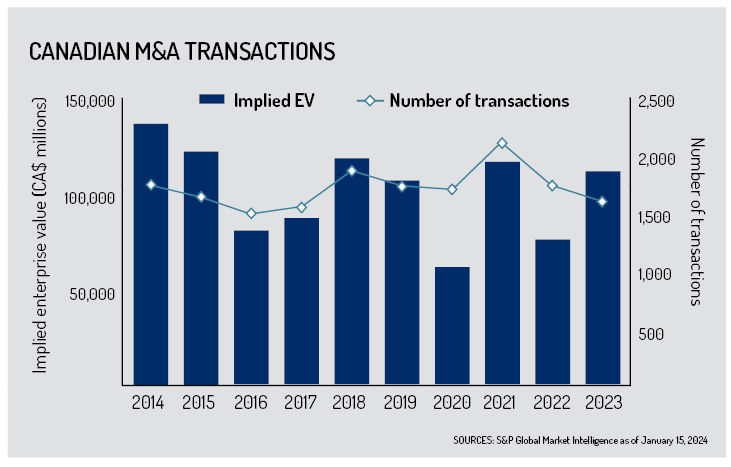

As we settle into 2024, the question on the minds of M&A lawyers in Canada is whether there is reason for optimism on dealmaking this year. After all, Canadian mergers and acquisitions lagged in 2023 compared to the previous two years, primarily fuelled by the impact of higher interest rates and the uncertainty around when they might fall.

The volatility from that uncertainty led to concerns over valuations and financing, says Angela Blake, Toronto-based partner at Bennett Jones LLP. This, coupled with “macro headwinds” such as a tense geopolitical climate and inflation, helped create a substantial downturn in overall M&A activity in 2023. And many of those factors are still in play today.

Says Blake: “The higher interest rates increased borrowing costs and made it more difficult for buyers to find financing, especially if you had to borrow from more than one lender.”

Still, even in that uncertain climate, she points to bright spots in sectors such as utilities, energy, and mining, especially critical minerals and clean energy.

Blake gives several reasons for optimism, including the stabilization of interest rates and inflation numbers, so dealmakers are more comfortable about the environment in which they are working; more growth in private credit-backed transactions; ongoing interest in renewables, energy, and resources; and the potential increase in restructuring and distressed M&A opportunities in a post-COVID world.

“Even the fact that people are pretty comfortable in thinking that rates won’t go higher – and will likely come down – has reduced the uncertainty keeping dealmakers on the sidelines.

“We have a lot of people that have been sitting on the sidelines for a long time,” Blake adds, with “a lot of capital” to deploy. “I think 2024 will be an improvement over last year.”

Blake’s colleague in Calgary, Ashley White, co-head of the energy practice at Bennett Jones, agrees. She says that while the deal count in 2023 was slower overall, M&A in utilities and the oil and gas sectors picked up in Q3 and Q4.

She anticipates a year like 2023 – a relatively slow start but gaining momentum as the year progresses. White notes that “several traditional oil and gas companies are experiencing increased cash flows – that gives them more opportunity to develop strategies, including using M&A to deal with the coming energy transformation.”

The size of the Canadian oil and gas industry means there is limited scope for large acquisitions compared to deals to be made in the US. Still, White anticipates that consolidation will continue, with small and mid-cap companies the likely targets for strategic acquirers and investors in 2024, particularly in light of ample fossil fuel reserves, high commodity prices, and improving market access.

She also says that M&A activity in the sector will continue to balance investments for both efficiency and decarbonization.

White says there are also significant opportunities for M&A in the renewable energy space, with increasing foreign interest in Canadian projects. She adds there may also be cross-sector transactions related to renewable energy, with Original Equipment Manufacturers looking to secure critical minerals needed for battery production and energy storage and continued interest in hydrogen and ammonia as well as wind and solar projects.

In the tech sector, Brigitte LeBlanc-Lapointe, a partner with Norton Rose Fulbright Canada LLP in Ottawa, notes that dealmaking was negatively impacted by the sudden collapse of Silicon Valley Bank in March 2023, further increasing what was already a lag in M&A.

Despite that turbulence, LeBlanc-Lapointe says certain tech subcategories – artificial intelligence, clean tech, critical minerals, and renewables – attracted interest from investors and acquirers in 2023, a trend likely to continue into 2024.

Government interest in the tech sector will also help, including a new federal clean tech investment tax credit and a tech talent strategy to address the scarcity of highly skilled workers. She says such initiatives will help “nurture attractive M&A targets.”

She adds there will also be more talent-driven M&A – or “acquihires” – allowing a buyer to gain another company’s employees to fill talent gaps.

LeBlanc-Lapointe concludes that 2024 “could be an exciting year in Canadian tech M&A,” especially in the small-to-mid-cap space, where players have spent the last few years on the sidelines. Market conditions will favour tech buyers with solid balance sheets and “strategic” buyers from other sectors looking to leverage technology in their operations or offerings.

While prospective sellers in the tech sector have been waiting for the high valuations of a couple of years ago to return, they may now be willing to accept lower, “more realistic” valuations because they may no longer have the cash flow with limited access to venture capital.

Artificial intelligence will figure significantly in tech M&A activity, says LeBlanc-Lapointe, but not only among companies with AI capabilities as buyers and sellers. “In a general sense, buyers in various sectors are starting to leverage AI in their internal processes to source targets, evaluate them, and then conduct due diligence.”

Aaron Atkinson, a partner in the Toronto office at Davies Ward Phillips and Vineberg LLP, observes that the results for M&A in 2023 were “probably better than what people thought at the beginning of the year.” The same is likely to happen again in 2024.

However, uncertainty remains. While central banks, including the Bank of Canada, have indicated that rate cuts should be coming this year, Atkinson notes potential buyers and sellers are reassessing whether we will get those interest rate cuts sooner than later.

“I think there are a lot of people waiting for rate cuts to happen because once those costs come down, lending costs come down, and that can have a cascading effect,” he says. “And I think then you may see a lot of buyers start to dive in, particularly among financial buyers, because they’re the ones that rely on leverage to do their deals,” benefiting from lower interest costs.

Atkinson says there is still some hesitancy on the buyers’ part for jumping in too soon. “You don’t want to be the one that cuts a deal before the interest rates get cut. That’s the uncertainty right now.”

He describes “two camps” of sellers – companies with “heads still in the pandemic valuation” space and others that may be financially distressed “or getting there.”

As for buyers, private equity may be sitting on a lot of cash but are looking for financial return, and “there’s only so much they are willing to pay without blowing their financial models.” Despite having this “dry powder,” Atkinson says private equity deals still rely on a fair bit of debt to finance a transaction.

On the other hand, strategic buyers may buy for different reasons, such as synergies. Strategics are also willing to use company shares as “currency” for the transaction. He says that such currency, like exchangeable shares, is becoming popular in private equity deals and is one way for founders to keep skin in the game.

Tim McCormick, Toronto-based partner with the national corporate and capital markets practice at Borden Ladner Gervais LLP, says that while interest rates are higher than historic lows, companies can now better model a deal structure.

“There is just more conviction in the market that rates are going to be flat to lower,” McCormick says, “which is helpful for determining the valuations that deals will be done at.” He’s already noticed that debt markets are less tight than they were this time last year, “and this bodes well for M&A activity.”

While small-and-mid-cap deals ($100 million to $200 million) will likely do well, McCormick sees few mega-deals (like the Rogers-Shaw deal) getting done under current conditions. He considers the stricter competition laws and other regulations that have come into play, making it harder to get such big-ticket deals done, with buyers facing increasing regulatory burden and risk when going into such transactions without clearly knowing where they stand.

Still, there is geopolitical uncertainty – and not just because of Russia’s invasion of Ukraine and the war resulting from the Hamas attack on Israel. This year will be a record year for the number of people eligible to vote in nationwide elections – four billion, or half of the world’s population. (The Economist counts 76 countries where the eligible population can vote, including the United States, India, Russia, and the European Union.)

McCormick says the potential for any of these elections to destabilize is real, including perhaps the most critical foreign election for Canada – the US presidential election. Given that the US is Canada’s largest trading partner, McCormick says, “We do run into some political uncertainty as we get closer to November.”

Largest transactions with Canadian party in 2023

- Rogers Communications’ purchase of Shaw Communications ($26.5 billion)

- British Columbia Investment Management Corp. and MacQuarrie Asset Management’s acquisition of United Kingdom’s National Grid Gas ($18.6 billion)

- Canada Pension Plan Investment Board and Silver Lake Technology Management purchase of Qualtrics from SAP ($15 billion)

- Brookfield Corporation, Cameco Corp., and Brookfield Renewable Partners’ acquisition of Westinghouse Electric Co. ($11.4 billion)

- British Columbia Investment Management Corp. and Advent International’s purchase of Maxar Technologies ($9 billion)

SOURCES: S&P Global Market Intelligence, Kroll

***

Aaron Atkinson, Davies Ward Phillips & Vineberg LLP

Angela Blake, Bennett Jones LLP

Ashley White, Bennett Jones LLP

Brigitte LeBlanc-Lapointe, Norton Rose Fulbright Canada LLP

Tim McCormick, Borden Ladner Gervais LLP