Banks are an important player in the economic stability of any government. In Canada though, preference is given to wholly domestic banks. This is why banks are categorized as Schedule I, Schedule II, and Schedule III banks. This helps the government partition the rights and obligations enjoyed by each bank, depending on their status.

But what exactly distinguishes one from the other? This article will help highlight schedule II banks and their role in the overall financial status of Canada.

What is a Schedule II bank?

To preface, the “Schedule” system of categorization has gone through changes. Due to its popularity, however, the term is still being used to classify banks despite restructuring. For the purposes of this article, we will be discussing Schedule II banks as was previously defined.

Schedule II banks are subsidiaries of a foreign bank. They are domestic but have ties with foreign financial institutions. Does that mean they’re the same entity as the foreign bank? Not really. Schedule II banking companies are their own entities. This distinction is important when considering its governing laws, compliance issues, and even taxes.

Here’s an explainer about Schedule II banking corporations in Canada:

These banks may take deposits from depositors and engage in other transactions expected of banks. In fact, they’re governed by the Bank Act with certain limitations because of their classification.

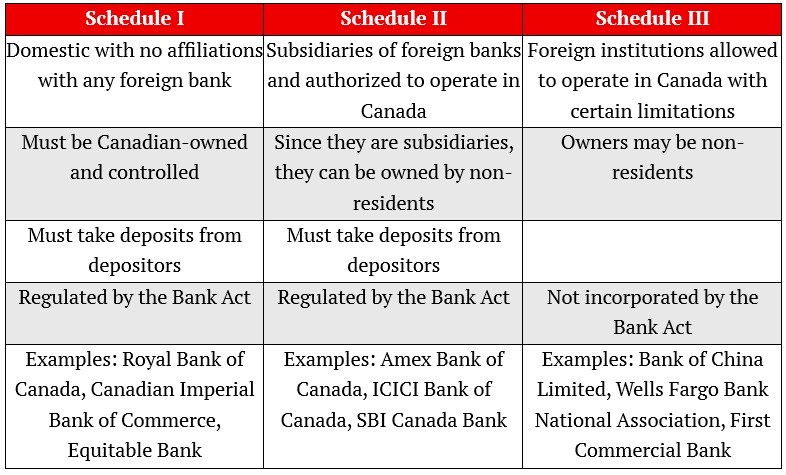

Differences between Schedule I, II and Schedule III banks

The difference between Schedule I, II, and III banks lies primarily in their ownership. By extension though, this also limits the kind of banking activities they can do. As indicated in the chart below, Schedule I banks have more freedom with their transactions while Schedule II and Schedule III banks have more restrictions.

Typically, Schedule II banks have more targeted services where they cater to specific industries as opposed to the full service of Schedule I banks.

To repeat – restructuring of banks created new classifications. While the schedule system remains to be popular, Canadian laws created a new method of categorization. The schedule system based its classification on residency status, but the new system is based on equity.

Ownership and control of Schedule II banks

So how does the new classification work? Under Bill C-8, which passed in 2001, equity determines the extent of foreign ownership allowed for banks. Here’s a chart about how this works:

|

Bank size |

Measure of equity |

Ownership restrictions |

|---|---|---|

|

Small banks |

If banks have an equity of less than $1 billion |

No restrictions |

|

Mid-sized banks |

If banks have an equity of more than $1 billion but less than $5 billion |

There must be a public float of at least 35 percent of voting shares |

|

Large banks |

If banks have an equity of more than $5 billion |

No single person must have more than 20 percent of the voting shares or for non-voting shares, not more than 30 percent |

Based on this, foreign entities can now buy into small banks and even own a substantial number of shares. They can even control these banks if enough shares are purchased. This essentially abandons the “widely held” principle previously adhered to by Canadian law. The widely held principle used to limit single ownership to just 10 percent of the voting shares.

For mid-size and large banks, restrictions are still in place. For Schedule II banks, the rules are more lenient because it only requires a public float of 35 percent. This means that at any given time, at least 35 percent of the voting shares must be available for public trading. The remaining voting shares may be held by insiders or major shareholders.

Have questions about cross-border banking laws? You can reach out to our Lexpert-ranked best cross-border lawyers and law firms in Canada for answers.

Read next: How to issue shares in a corporation in Canada: A step-by-step guide

Regulatory oversight of Schedule II banks

Schedule II banks are primarily regulated by the Bank Act. However, they must also follow other laws such as those for money laundering, data breach laws, deposit insurance, and others. Schedule I and Schedule II banks have similar regulatory bodies which includes:

- Office of the Superintendent of Financial Institutions (OSFI)

- Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)

More departments are, of course, involved in regulating Canadian banks. The regulations are constantly evolving, which requires banks to have a dedicated team to keep up with the changes. This is especially true for OSFI-issued regulations, which tend to change on a routine basis depending on economic indicators.

Legal requirements for licensing and operation

Establishing any bank in Canada requires undergoing rigorous licensing and permitting requirements. Often however, it starts by getting Letters Patent from the Finance Minister for incorporation. The OSFI must also issue an order authorizing the start of business operations.

Typically, the process of opening a bank can be divided into three phases:

|

Phase 1 |

This is the pre-application phase where the applicant meets with OSFI authorities to discuss the application. Applicants will also submit requirements, which will be reviewed by OSFI before issuing a preliminary report on the application. |

|

Phase 2 |

This involves publishing a notice of intent to apply for letters of patent. This must be done in three consecutive weeks in a newspaper of general circulation and in Canada Gazette. OSFI will review the formal applications and then submit its recommendation to the Minister. |

|

Phase 3 |

If the Minister issues a letter of patent, OSFI will conduct another review of the application. Further meetings may be asked until OSFI is satisfied in which case, an order to commence will be issued. |

Additional requirements such as membership with the Canada Deposit Insurance Corporation is also required.

Limitations, compliance, and reporting obligations

Banks have stringent reporting and compliance requirements. This is doubly so for those classified as Schedule II because as subsidiaries of foreign banks, they may deal with cross-border transactions more often than domestic banks.

Limitations on Schedule II banks

Here are some of the limitations imposed on Schedule II banks by the Bank Act:

- They cannot deal in goods, wares, merchandise, or in any other trade or business

- Acting as a trustee or taking part in fiduciary activities

- Leasing of personal properties, including automobiles

- Engaging in the business of insurance beyond what is allowed under the Bank Act

Compliance and reporting

Compliance with the Bank Act and other laws can often be complex because there is not a single guide available to banks. Instead, several laws are in place which need to be read together to ensure compliance.

Here's a small snapshot of the compliance and reportorial measures required from banks:

Capital reserve

All banks need to maintain a capital reserve according to OSFI regulations. This capital reserve is meant to ensure that banks will continue to operate despite changes in the economic climate. The amount in the reserve is often set by OSFI after calculations and may change from time to time.

Financial disclosures

Financial disclosures involve reporting certain balances of the bank to OSFI. This can include allowance for expected credit losses, home equity line of credit, income statement, leverage requirement returns and others. These reports are often done annually or quarterly, depending on OSFI.

This continuous generation of reports is often the bane of many banks. A dedicated team is often tapped to make sure the reports are completed and filed on time. Under OSFI rules, erroneous or late reports can expose the bank to administrative penalties.

Security measures

Banks have the obligation of ensuring that financial transactions coursing through them are all lawful. This is often covered by laws on money-laundering and terrorist financing which compels banks to know their clients. The goal of the law is to ensure that suspicious transactions are reported so that the unlawful movement of money may be stopped.

Since the very nature of banks gives them access to money transactions, the law imposes an obligation on them. In fact, penalties may be placed on banks that do not comply with the law. For example, FINTRAC, the agency responsible for money laundering regulations, has issued a $2 million penalty on the Exchange Bank of Canada.

Reporting of security breaches

Banks are also mandated to set up security features to protect the personal information of their clients. In case of breaches, they must inform clients about the breach as soon as possible. Failure to do so can make the bank liable for penalties as well. The Bank Act also contains prohibitions against disclosure of personal information.

Here’s some information about how data breaches should be notified to the affected data owners:

Tax implications for Schedule II banks

When it comes to corporate tax payments, the laws recognize resident and non-resident taxpayers. For purposes of paying taxes, Schedule II banks are resident taxpayers. This is because they are incorporated under the laws of Canada and are distinct entities from the parent corporation.

This means that their income tax is based on worldwide income as opposed to income derived from Canada operations only. Note that treaties may take effect in these instances, allowing banks to essentially cancel reciprocal taxes. This helps prevent double taxation, especially for corporations that transact across borders.

Best practices for banks

Ultimately, Schedule II banks are covered by the Bank Act and have the same obligations as Schedule I banks. With the restructuring, however, the distinction between Schedule II and Schedule I has become blurred. This makes it doubly important for banks to engage in the services of excellent banking lawyers in Canada to help them harmonize the changes.

Other best practices of banks include:

-

Having good corporate governance. This means having a strong corporate structure complete with published policies that employees can follow to guarantee compliance

-

Having a dedicated team that deals with different aspects of operation such as a data privacy branch, reportorial branches, accounting, and so on. This guarantees that all aspects of branch operation are given proper attention

-

Transparency with reports to ensure that all stakeholders have the information they need when making decisions. These efforts should include a timely reportorial, especially for financial statements published for shareholders

Of course, compliance measures must also include the different regulations imposed by provincial authorities. For example, British Columbia has the Financial Institutions Act which is applied on banks operating in British Columbia.

Bank Act is one of the banking laws in Canada, get to know some of the must-know rules for consumers in this guide.

Do you want a targeted approach to your questions? Check out some of the best banking lawyers in British Columbia for your precise answers.