Before Bill C-8, banks were characterized as Schedule I, Schedule II, and Schedule III banks. Today, however, banks are classified based on the value of their equity. Does that mean that the “schedule” system has been abandoned? Not necessarily. The Bank Act still identifies banks using the “schedule system.”

For this reason, the definition and distinctions between Schedule I, II, and III banks still matter for purposes of compliance with relevant laws. In this article, we’ll talk about Schedule III banks and how they operate in relation to Canada’s banking laws.

What is a Schedule III bank?

Schedule III banks are a special breed of banks operating in Canada. They are essentially branches of foreign banks – making them foreign-owned as opposed to Schedule I banks. They are not incorporated through the Bank Act, which means certain restrictions apply.

Differences between Schedule I, II, and III Banks

Here’s a more detailed look at the differences between schedule iii, ii, and i banks. Note that schedules I and II are similar while schedule III is a clear outlier.

|

|

Schedule 3 |

||

|---|---|---|---|

|

Category |

Domestic banks with no affiliations with any foreign bank |

Subsidiaries of foreign banks and authorized to operate in Canada |

Foreign institutions allowed to operate in Canada with certain limitations |

|

Ownership |

Must be Canadian-owned and controlled |

Can be owned by non-residents |

Owners may be non-residents |

|

Deposits |

Must take deposits from depositors |

Must take deposits from depositors |

|

|

Regulation |

Regulated by the Bank Act |

Regulated by the Bank Act |

Not incorporated by the Bank Act |

|

Examples |

Royal Bank of Canada, Canadian Imperial Bank of Commerce, Equitable Bank |

Amex Bank of Canada, ICICI Bank of Canada, SBI Canada Bank |

Includes Bank of China Limited, Bank of America, Capital One, Wells Fargo Bank National Association |

Simply put Schedule II banks have foreign ownership but are incorporated in Canada through the Bank Act. Schedule III banks have foreign ownership but are not incorporated through the Bank Act. Both Schedule II and Schedule III banking corporations are a way for foreign banks to operate in the country.

As mentioned, restructuring in the classification of banks has created new categories. Under Bill C-8, here’s the new way of looking at banks:

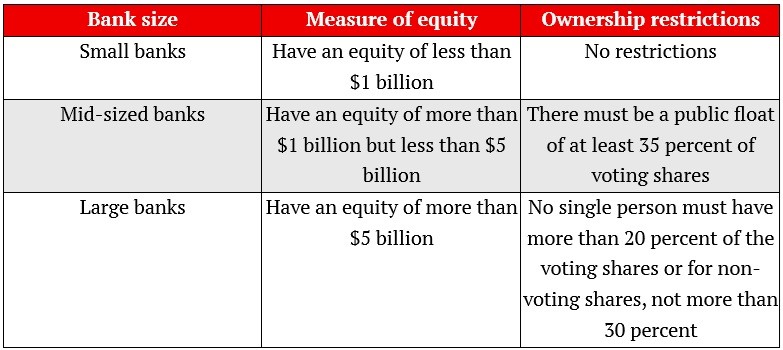

From the table, Canada now identifies banks according to the size of the equity so that small banks no longer have a restriction as to who can own how many shares.

Differentiating between schedule and equity

So, what’s the difference between the schedule system and the equity system? The primary distinction is ownership structure. Through the schedule system, the law adheres to the “widely held” principle. This means that stocks of Schedule I banks should be majorly owned by Canadian residents.

In fact, under the widely held principle, a single entity cannot own more than 10 percent of a bank’s voting shares. This is no longer the case. Entity in this context includes corporations so that even corporations cannot own more than 10 percent of a bank’s shares.

Now though, the ownership of voting and non-voting shares depends on the size of the bank. Small banks or those with less than a billion in equity could now be bought by a single person. This means that control can be held by a single entity when it comes to small banks.

For mid-size banks, the requirement is a 35 percent public float of voting stocks. This means that at least 35 percent of the mid-sized bank’s voting shares should be available for trading with the public. Large banks on the other hand have a limit of 20 percent voting shares for a single entity. This increases 35 percent for non-voting shares.

Read next: How to issue shares in a corporation in Canada: A step-by-step guide

Legal and regulatory framework for Schedule III banks

Just because Schedule III banks are not incorporated through the Bank Act does not mean they are exempt from the laws. These banks are still subject to regulations issued by pertinent departments of the Canadian government.

Specifically, the regulations and compliance requirements issued by the Superintendent of Financial Institutions (OSFI) must be met. Reports must still be filed on time and free of any errors or omissions. This is because despite the foreign aspect of the bank, their operation is still filled with public interest, giving the Canada a measure of control.

Aside from OSFI regulations, the following obligations are still imposed on these banks:

-

Compliance with laws governing anti-money laundering and terrorist financing. Due to the nature of their operations and cross-border transactions, Schedule III banks may need to have more policies in place to ensure that the bank is not used for nefarious means

-

Compliance with data protection policies and reporting requirements. This means taking care of personal information of clients and immediately notifying them in case of breach

-

Compliance with OSFI regulations when it comes to policies affecting financial transactions such as debt-to-income ratios, mortgages, and equity requirements

-

Operational risks guidelines released by OSFI should also be taken seriously by banks, especially when it comes to crypto transactions

Can you transition from Schedule II to Schedule III bank?

Transitioning from Schedule III to Schedule II banks or vice versa isn’t often done. The difficulty lies in the fact that one is incorporated under the Bank Act while the other is merely authorized by the government.

For this reason, transitioning often means ending the existence of one so that another may be created. For example, Schedule III may be closed so that Schedule II may take its place or vice versa. The complexity of the transaction often requires the input of excellent cross-border lawyers who have a firm grasp of banking laws.

Bank Act is one of the banking laws in Canada, get to know some of the must-know rules for consumers in this guide.

Licensing and operational requirements for Schedule III banks

Also known as “authorized foreign banks” or AFB, Schedule III banking companies undergo stringent regulatory guidelines before being approved to operate in Canada. Because of their unique character, these banks have clear restrictions even during operation.

The process of approval involves getting the nod of the Finance Minister and assent from the OSFI. Unlike schedule I and II banks, however, they may not always be members of the Canada Deposit Insurance Corporation. Why? The answer lies in how they operate.

Read next: What it takes to get a bank license in Canada

Limitations of Schedule III bank activities

Schedule iii banking companies do not take retail deposits. Their offering is on a wholesale basis, which means that their services are offered to larger entities. Here’s a nice explanation differentiating wholesale and retail banking:

This limitation means that Schedule III banks are not in direct competition with other banks. The size and cross-border nature of the bank also gives it more resources in catering to larger clients. Foreign authorized banks are also prohibited from dealing in securities in the following cases:

-

Securities are dealt as primary distribution of shares or ownership interests

-

Securities dealing consist of secondary market trading of shares or ownership interests

-

Securities dealing involves acting as a selling agent with respect to mutual funds distribution

-

Securities dealing is primarily for the distribution of debt obligations of a corporation

Tax and cross-border implications for Schedule III banks

When it comes to taxes, banks may be classified as residents or non-residents. Residents are taxed for income generated worldwide while non-residents are only taxed for income generated within Canada. Authorized foreign banking corporations are considered non-residents. This means that the income of the parent corporation is rarely taxed.

Of course, certain treaties and agreements often exist when it comes to commercial transactions. Depending on the citizenship of the main bank, there may be cross-border laws that help harmonize the payment of taxes. Reciprocal benefits may be available so that banks can avoid double taxation across different jurisdictions.

Best practices of Schedule III banks

The unique characteristic of authorized foreign banks means that their best practices take their foreign status into consideration. The goal of these banks is to align their operations with Canadian regulations while harmonizing with their country of origin. The most obvious aspect where clashes can happen is through taxes.

With the right approach however, Schedule III banks can successfully operate within and without Canada. In fact, many banks have been doing so for years – and thriving while contributing to Canada’s financial health. Here are some of the best practices available to banks when it comes to operations:

Good corporate governance

Everything starts with good corporate governance. Even authorized foreign banks have directors, managers, or operational leaders that create policies for day-to-day operations. For foreign banks operating through branches, having policies in place helps prevent breaks in communication.

Good corporate governance is something that’s built from the ground up. It starts early during the commencement of the business and should be constantly updated depending on climate change. It also involves constant updates to existing policies through the input of experts in the field.

For more information about corporate governance, this video should add some context:

Transparent intra-corporate reporting

Intra-corporate reporting refers to reports within the organization itself. This is critical for authorized foreign banks because the extent of the organization can quickly lead to communication breakdown. Intra-corporate reports mean that the principal bank is kept up to date in all the transactions of the branch.

Keep in mind that the authorized foreign bank is essentially taking orders from the parent bank. This means that any developments, especially with prevailing regulations, must be communicated immediately. Otherwise, even the parent bank may be involved in any administrative penalties imposed by OSFI.

Coordinating teams to harmonize compliance laws

In every organization, having a dedicated team for specific roles is a must. With foreign bank branches though, this element is even more important. This is because multiple factors are moving all at once. There are the laws of the parent corporation and laws of the branch bank intersecting with each other.

Routine meetings, updates, and teams that coordinate smoothly with each other help prevent any gaps in compliance.

Authorized foreign banks come with a layer of complexity that’s literally beyond borders. This means that having a dedicated team for the foreign authorized bank in Canada is critical. At the same time, a dedicated team in the home country should also be present with the two teams consistently talking to each other for cooperation.

If you want to find out more about Schedule III banks and financial institutions in Canada, you can targeted help from Lexpert-ranked best banking lawyers practicing in the area today.